CDSL: Can Demat Account Dominance Sustain Margins Amid Regulatory Fee Compression and NSDL Competition?

CDSL controls 80% of India's demat accounts with 17.27 crore accounts, but SEBI-driven fee compression and NSDL's IPO-fueled competitive push challenge its premium valuation at 50x P/E.

CDSL: Can Demat Account Dominance Sustain Margins Amid Regulatory Fee Compression and NSDL Competition?

What You Can Do Next

- Read the full article for complete insights

- Save for later reference

- Share with others learning about this topic

Image not available

Central Depository Services (India) Limited (CDSL), the dominant depository in India with an 80% market share by demat accounts, occupies a unique monopoly-like position in the capital markets infrastructure. With 17.27 crore demat accounts as of Q3 FY26 and Rs 46,271 lakh crore in custody value, CDSL sits at the intersection of India's financialization megatrend. Yet its Q3 FY26 results reveal a tension: consolidated revenue grew 9.4% YoY to Rs 304 crore, but net profit inched up just 2% to Rs 133 crore, signaling margin headwinds. This analysis, triggered by its January 2026 earnings, goes beyond headline numbers to question whether SEBI's regulatory push on fee compression through mandatory Basic Services Demat Accounts (BSDA), rising compliance costs, and NSDL's post-IPO competitive ambitions can erode the structural advantages that justify CDSL's premium 50x P/E valuation. For Indian retail investors, the core debate is whether market structure moats are truly permanent or slowly narrowing.

Frequently Asked Questions

Why does CDSL trade at such a high P/E ratio compared to other financial infrastructure companies?

CDSL operates as a near-monopoly in depository services with 80% market share, zero debt, high margins (45%+ net margin), and direct exposure to India's financialization trend. The premium reflects its asset-light model and recurring revenue streams. However, the 50x P/E assumes sustained 15-20% earnings growth, which faces headwinds from fee regulation.

How does SEBI's BSDA mandate affect CDSL's revenue per account?

SEBI requires all new individual demat accounts to be Basic Services Demat Accounts with zero AMC for holdings up to Rs 4 lakh and only Rs 100 for Rs 4-10 lakh. This structurally lowers revenue per account as the proportion of BSDA accounts grows, pressuring CDSL to rely more on transaction fees and KYC/data services.

Is NSDL a real competitive threat to CDSL?

NSDL holds 20% of demat accounts but dominates institutional custody. Post-IPO, NSDL has capital to invest in technology and DP acquisition. While switching costs in depository are high, NSDL could capture incremental growth in Tier 2-3 cities where CDSL's retail dominance was built.

References

- [1] CDSL Q3 Results FY2026: Net profit up marginally to Rs 133 crore, revenue climbs 9% - ET Now. View Source ↗(Accessed: 2026-02-19)

- [2] CDSL Q3 FY26 Earnings Call Transcript - AlphaStreet. View Source ↗(Accessed: 2026-02-19)

- [3] CDSL Q3 FY26 Financial Results: Standalone and Consolidated - Prysm. View Source ↗(Accessed: 2026-02-19)

- [4] CDSL Depository Tariff Structure - CDSL India. View Source ↗(Accessed: 2026-02-19)

Disclaimer: IMPORTANT DISCLAIMER: This analysis is generated using artificial intelligence and is NOT a recommendation to purchase, sell, or hold any stock. This analysis is for informational and educational purposes only. Past performance does not guarantee future results. Please consult with a qualified financial advisor before making any investment decisions. The author and platform are not responsible for any investment losses.

Continue Your Investment Journey

Discover more insights that match your interests

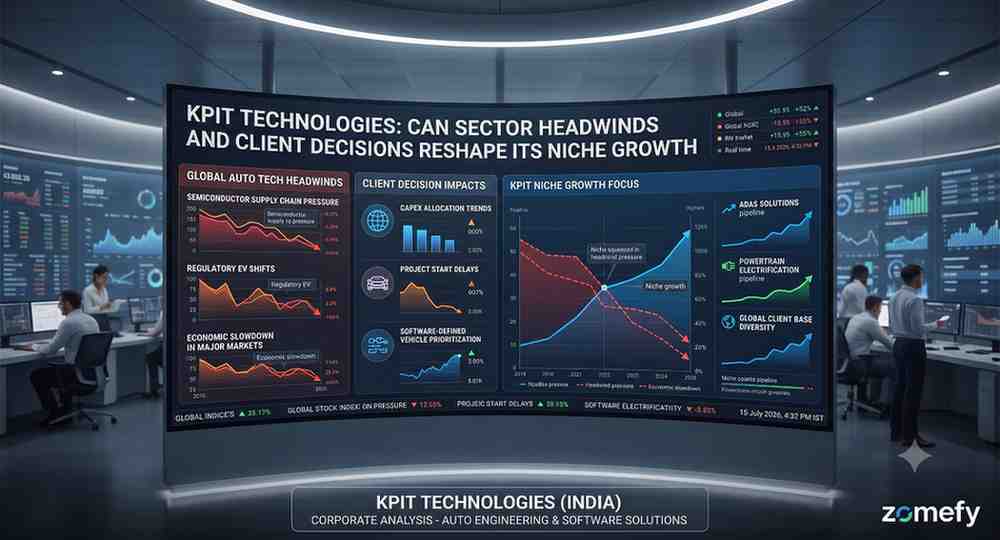

KPIT Technologies: Can Sector Headwinds and Client Decisions Reshape its Niche Growth

KPIT Technologies, an Indian IT services firm specializing in the automotive and mobility sector, has carved out a niche in the global software-defined vehicle (SDV) landscape.

Flipkart 2025: Walmart-Backed E-commerce Giant's $40B IPO Path and Profitability Pivot

Flipkart's move from a Singapore holding structure back to India is the prologue to what could be the marquee listing of India's next new-economy wave: a Walmart-backed Flipkart IPO targeting a hea...

Pidilite Industries: Can Premiumization Strategy Sustain Margin Expansion Amid Rising Competition?

Pidilite Industries, a household name in India synonymous with adhesives like Fevicol, has long been a darling of the Indian equity market, celebrated for its strong brand recall, extensive distrib...

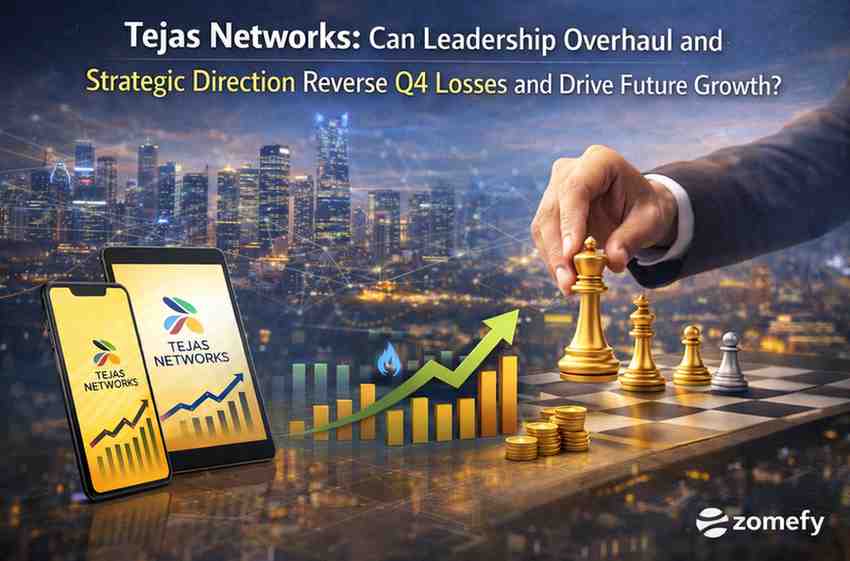

Tejas Networks: Can Leadership Overhaul and Strategic Direction Reverse Q4 Losses and Drive Future Growth?

Tejas Networks Limited (NSE: TEJASNET, BSE: 540595) stands at a critical juncture, navigating a challenging phase marked by significant financial losses and a strategic leadership overhaul.

Explore More Insights

Continue your financial education journey